Who are Home Buyers in the North Port Area in 2025? Why It Matters If You're Selling

Who’s Buying Homes in North Port, Florida in 2025, and Why It Matters If You’re Selling Curious who’s snapping up homes in North Port right now — and how that shapes your chance to sell fast? Today’s North Port buyers are cash-rich retirees relocating from high-tax states like Ohio, Michigan, and Ne

Read More

Buy Now or Wait for Spring? What North Port Homebuyers Need to Know

How to Sell and Buy a Home Seamlessly in North Port — Timing, Strategy & What to Know Selling and buying a home at the same time in North Port and the surrounding areas is achievable when you have a clear plan based on real market data. In 2025, single-family homes that are 1,300 square feet or la

Read More

What Are Today’s Most Effective Seller Incentives (Beyond Price Cuts)

What Are Today’s Most Effective Seller Incentives (Beyond Price Cuts)? If you're looking to buy a home in Port Charlotte, Florida, you’ll find that many sellers are now using tools beyond simply lowering the price. This page explains how sellers are motivating offers with creative incentives — and h

Read More

Your Ultimate Guide to Buying a Home in Florida: Beyond the Sunshine

Your Ultimate Guide to Buying a Home in Florida: Beyond the Sunshine Florida's sunshine comes with strings attached – and smart home buyers know exactly what to look for. Are you prepared for the hidden realities of the Sunshine State's real estate market? Unlocking Your Florida Dream Home: A Compre

Read More

Ten Essential Steps to Buying a Home in North Port, or Venice Florida

Ten Essential Steps That Actually Work (From Someone Who's Been There) I'll be honest with you – buying a home in North Port, Venice, Englewood, or anywhere in our beautiful Sarasota County area can feel overwhelming. Trust me, I've walked alongside hundreds of families through this journey, and I'v

Read More

Your First Home in Paradise: A Complete Guide to Buying Your First Home in North Port, Venice, and Englewood, Florida

Your First Home in Paradise: A Complete Guide to Buying Your First Home in North Port, Venice, and Englewood, Florida Published: August 2025 The dream of owning your first home in Southwest Florida has never been more attainable. While national headlines focus on market uncertainty, savvy first-

Read More

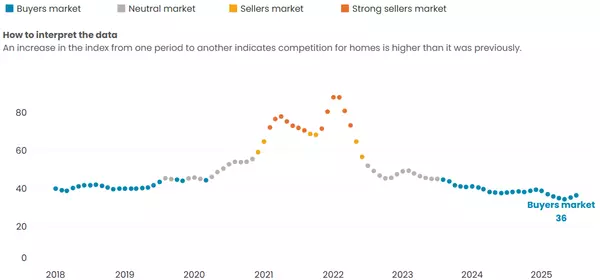

Top Buyers Market Across the U.S. - North Port Florida near the top

The top buyer’s markets across the U.S. right now are, according to a recent article by Zillow, with North Port, Florida, near the top spot. Knowing the neighborhoods in the local Florida markets is key to understanding what this means to your specific property. Home buyers are not going to overp

Read More

Why Overpricing Your North Port Home Can Cost You $20,000+ (And What Venice & Port Charlotte Sellers Need to Know)

Why Overpricing Your North Port Home Can Cost You $20,000+ (And What Venice & Port Charlotte Sellers Need to Know) Last Updated: July 24, 2025 | Southwest Florida Real Estate Market Analysis As a Southwest Florida real estate expert who has successfully sold over 100 homes in North Port, Venice, and

Read More

Real Reasons Why People are Moving in 2025

What are the real reasons people are moving in 2025? The top answer may surprise some of you, while others will completely agree. Moving is not just a financial decision; it is also an emotional one. See this video for the top reasons people are choosing to move in 2025. Bill Bambrick is a North

Read More

Buy a Florida Home with a Pool or Build a Pool - Risk or Reward

Buy or build a Florida pool, risk or reward? In this video, we will unpack the pros and cons of having an inground pool from either an existing pool or considering building a pool with your home. As a North Port Florida realtor, there are many choices when buying a home, including whether you

Read More

How Do Climate Risks Affect Your Next Home?

Climate change is impacting where people buy homes. As the experts at the National Association of Realtors (NAR) explain:“Sixty-three percent of people who have moved since the pandemic began say they believe climate change is—or will be—an issue in the place they currently live.”If you’re planning

Read More

What’s Next for Home Prices and Mortgage Rates?

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.The only thing you can really do is make the be

Read More

Tips for Younger Homebuyers: How To Make Your Dream a Reality

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.While there’s no a

Read More

The Best Way To Keep Track of Mortgage Rate Trends

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.The problem is, with all the headlines in

Read More

Why We Aren't Headed for a Housing Crash

If you’re holding out hope that the housing market is going to crash and bring home prices back down, here’s a look at what the data shows. And spoiler alert: that’s not in the cards. Instead, experts say home prices are going to keep going up.Today’s market is very different than it was before the

Read More

Market Report North Port 34286 October 2023

This housing market report is for 34286 in North Port Florida. Brought to you by Bill Bambrick, LPT Realty.

Read More

Market Report 33981 Feb 2, 2024

This housing market report update is for zip code 33981 located in Port Charlotte Florida. The criteria are single-family homes 3 bedrooms and 2 bathrooms, no pool, any age of the property, and lot size. There are no lots included in this review. The data is all active listings to this date, pen

Read More

Categories

- All Blogs (385)

- Aging Parents (2)

- Best Realtor (2)

- Buyers Tips (46)

- Condos (2)

- Downsizing (8)

- Equity (5)

- FAQ (2)

- Financing/Mortgage (8)

- First Time Home Buyers (17)

- Fun Items (6)

- Heron Creek (1)

- Home Remodeling (7)

- homes near golf courses (1)

- Investing (4)

- Living In North Port (5)

- Local Housing Market (51)

- luxury homes (3)

- Making Offers (9)

- Moving (6)

- Multigenerational (5)

- New Construction (3)

- Nokomis Florida (1)

- Nokomis Housing Report (1)

- North Port Florida (5)

- North Port Housing Report (7)

- Pool Homes (3)

- Port Charlotte Florida, (2)

- Probate / Divorce / Foreclosure (1)

- Rent (2)

- Rotunda West (2)

- Sellers (52)

- south gulf cove (2)

- Thing to Do in the Area (8)

- Venice Housing Report (4)

- Venice, Florida (2)

- Waterfront Homes (2)

- Wellen Park (2)

Recent Posts